07.26.2024

Safe moderation

In the US, the cautionary approach introduced into our projected growth baseline has not yet been quantitatively incorporated into our forecast, but evidence of weakening consumer spending momentum is accumulating.

GROWTH

US – Under pressure

In the US, the cautionary approach introduced into our projected growth baseline has not yet been quantitatively incorporated into our forecast, but evidence of weakening consumer spending momentum is accumulating. As a result, we are revising our GDP growth outlook downwards for Q2 and anticipate downside risks for H2.

Recent data indicates that consumer spending prospects are declining. This is evidenced by the below facts:

1. Services activity lost direction. The ISM services index fell back into recessionary zone in June for the second time in the past three months. Weaknesses were widespread, affecting key subcomponents such as business activity, employment, and new orders. Although some recovery is likely in July, the increased volatility casts a shadow over the outlook for domestic demand.

2. The labour market is at a crossroads. On the one hand, JOLTS data for May suggests the current level of job openings is consistent with a balanced market.

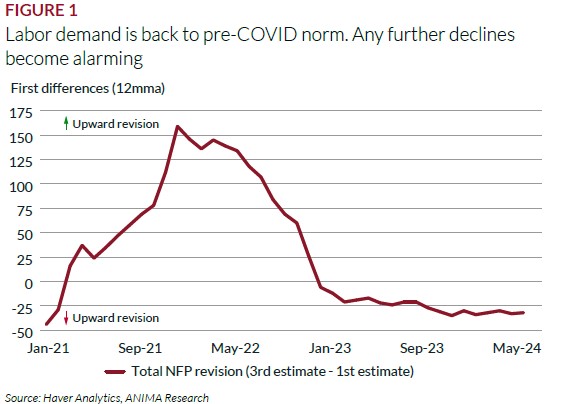

However, with key sub-indices such as quits rate, separation rate, hire rate, and openings/unemployed ratio being close to or below pre-pandemic levels, any further declines from these levels will become more alarming. On the other hand, the June non-farm payroll report highlighted two issues. Firstly, the data does not seem particularly reliable, with job creation being repeatedly overestimated and more than 111k jobs initially reported being retracted over time since April.

Secondly, the private sector is losing momentum in job creation, including in the manufacturing and services sectors. Over the past two months, non-cyclical and government jobs have seen sustaining job creation. (Figure 1)

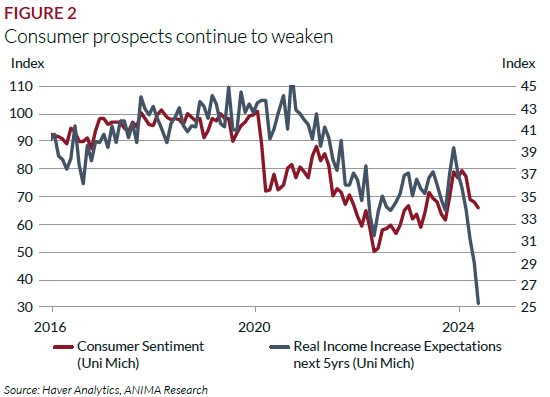

3. Consumer confidence keeps declining. (Figure 2)

4. Spending momentum is losing steam across the board. In May, the monthly growth rate of spending for services has dropped to its lowest level since August 2023.

ANIMA baseline. Against this backdrop, we revise down our GDP growth forecast for Q2 to 1.8% q/q SAAR (from 2.1% prior). For Q3-24 we expect 1.4% q/q SAAR (unchanged from previous baseline) and 1.4% q/q SAAR for Q4-24 (unchanged from previous baseline) – consistent with an annual growth rate of 2.3% (from 2.4% prior).

Download full document