03.22.2024

NOT GIVING UP

We remain TACTICALLY NEUTRAL and we suggest an opportunistic approach

Following the recent sharp rally, we remain TACTICALLY neutral on BTPs. For the following reasons:

A) BTPs are expensive vs. core, as well as vs. periphery

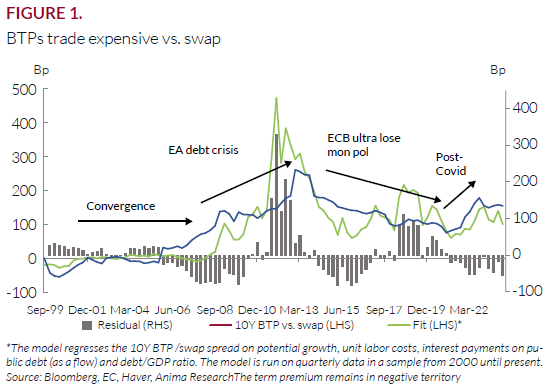

Figure 1 shows that according to macro fundamentals, 10Y BTPs should trade at a spread of 150bp vs. swap, around 50bp wider than current levels. Such negative residual was only observed at the beginning of QE in 2015.

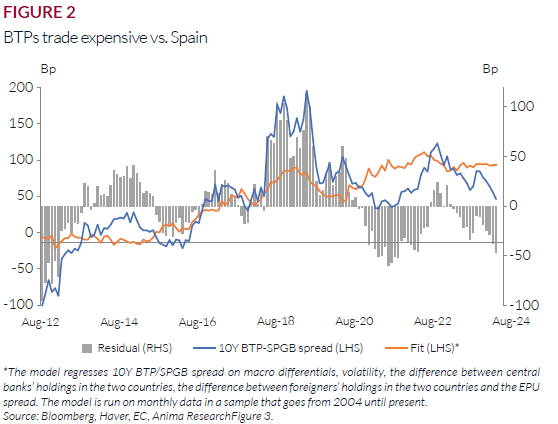

BTPs are also rich vs. SPGBs (Figure 2). Our fair value model indicates that the 10Y BTP-SPGB spread should trade at 95bp. It reached 45bp recently. In line with evidence from Figure 1, such negative residual was only observed in the first period of QE.

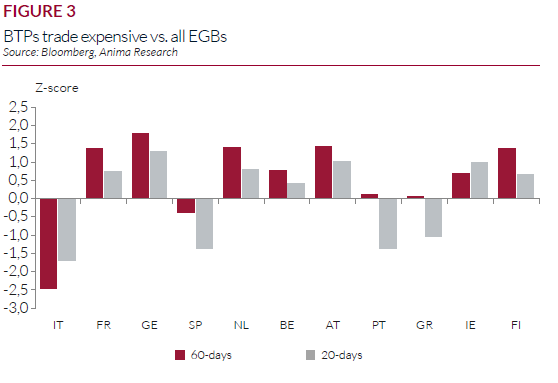

Last but not least, Figure 3 shows that, while in a near-term perspective (60-and 20-days Z-score) all peripheral countries trade somewhat expensive in spread vs. swap, Italian govies are by far the most expensive.

Chiara Cremonesi

Senior Rates Strategist

Investment Research