SLIGHTLY LONG TACTICALLY

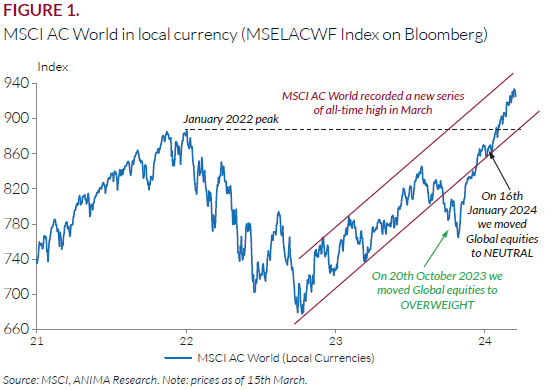

Global benchmark at new record high. The MSCI AC World rebounded c. 20% from last October’s lows reaching a new all-time peak (Figure 1). The rally was mainly led by a combination of declining nominal/real yields and better than expected macro developments.

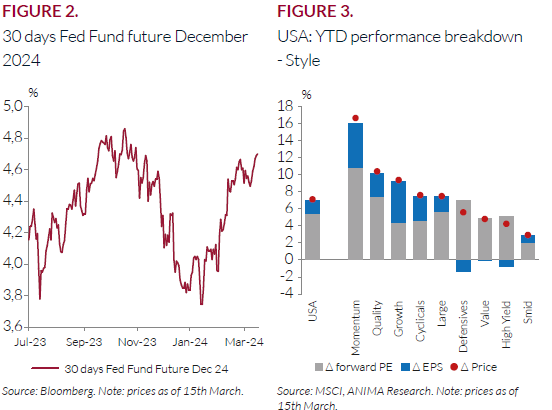

The rally continued despite the sharp market repricing of the Federal Fund Rate (FFR). At the end of December 2023, the rates market expected the FFR at 3.8% by December 2024; now it is forecasted at 4.6%. Such upward revisions did not hit the equity market. Focusing on the US, the star and stripes equity benchmark gained c.7% YTD, of which 5pp came for multiple expansion, and 2pp from EPS. Across the main style and the 24 sectors, only Growth names are grinding higher boosted supported by earnings rather than multiples (Figure 2 and Figure 3).

We turn slightly LONG tactically (NEUTRAL previously). The reason is four-fold: 1) our analysis, focused on US equities, shows as the ongoing market rally is broadening again; 2) earning revision indices turned positive suggesting that Q1 results may surprise to the upside once again; 3) despite the 20% rebound since the October lows the market looks fairly priced in under several metrics; 4) favorable seasonality.

Cosimo Recchia

Senior Equity Strategist

Investment Reserach